Course notes for “Stochastic Process”

2014 Fall

1. Motivation

Brownian motion can be thought of a symmetric random walk where the jumps sizes are very small and where jumps occur very frequently.

- Each jump size are

- The time before two jumps are

.

.

1.1 What’s the mean and variance?

Let

denote whether the i-th jump is to the right(+1) or to the left(-1), we have

with probability

and

respectively.

Thus,

![E[X_i] = 0](http://mytechroad.com/wp-content/ql-cache/quicklatex.com-f8aaebca6a792a3c1f96703c49cc3f67_l3.png "Rendered by QuickLaTeX.com")

and

![Var[X_i] = E[X^2_i] - E[X_i]^2 = 1](http://mytechroad.com/wp-content/ql-cache/quicklatex.com-1b4a23e17c1ffe9311f56a51f18e7bb9_l3.png "Rendered by QuickLaTeX.com")

.

Let  denote the state of Markov Chain after n jumps, then

denote the state of Markov Chain after n jumps, then

The  denote the continuous Markov Chain after n jumps, then

denote the continuous Markov Chain after n jumps, then

Then we have

![E[X(t)] = 0](http://mytechroad.com/wp-content/ql-cache/quicklatex.com-5521d8e7a8c3e27e09dae171218efa5f_l3.png "Rendered by QuickLaTeX.com") and

and ![Var[X(t)] = (Delta x)^2 cdot frac{t}{Delta t}](http://mytechroad.com/wp-content/ql-cache/quicklatex.com-0f44ab27f24a965379568a8548d9ea92_l3.png "Rendered by QuickLaTeX.com") .

.

Let  , then

, then

![V[X(t)] = (Delta x)^2 cdot frac{t}{Delta} to sigma^2 t](http://mytechroad.com/wp-content/ql-cache/quicklatex.com-fb1f4cf9dd65e73704e883268ac9c80c_l3.png "Rendered by QuickLaTeX.com") .

.

2. Properties of Brownian Motion

Answer: by the stationary property, we have

~

.

3. Standard Brownian Motion (SBM)

4. Brownian Motion with Drift

Definition 1: Let  be the standard Brownian motion. Let

be the standard Brownian motion. Let  , then is Brownian motion with drift

, then is Brownian motion with drift  .

.

Definition 2:  . is Brownian Motion with drift and variance parameter

. is Brownian Motion with drift and variance parameter  if

if

has stationary and independent increments

has stationary and independent increments- ~

Example: Let be Brownian motion with  and drift

and drift  . What is

. What is  Pr{X(30) >0 | X(10) = -3}

Pr{X(30) >0 | X(10) = -3} Pr{X(30) – X(20) >3 | X(10) =3 }Pr{X(30) – X(10) >3 }

Pr{X(30) – X(20) >3 | X(10) =3 }Pr{X(30) – X(10) >3 } Pr{X(20) – X(0) >3 }

Pr{X(20) – X(0) >3 } Pr{X(20)>3 }

Pr{X(20)>3 } Pr{N(2,80) > 3} = Pr{X(0,1) > frac{3-2}{sqrt{80}}

Pr{N(2,80) > 3} = Pr{X(0,1) > frac{3-2}{sqrt{80}} 1-Phi(frac{1}{4sqrt{5}})

1-Phi(frac{1}{4sqrt{5}}) X(s) = x | X(t) = B

X(s) = x | X(t) = B frac{s}{t} cdot B

frac{s}{t} cdot B frac{s}{t} cdot (t-s)

frac{s}{t} cdot (t-s) s = t/2

s = t/2 X(t)

X(t) N(0, sigma^2 t)

N(0, sigma^2 t) 10 after 6 hours, what is the probability that the stack was above its starting value after 3 hours?

10 after 6 hours, what is the probability that the stack was above its starting value after 3 hours?

Answer:

This is a Brownian bridge process where

~

=

.

Thus

Example 2: If a bicycle race between two competitors, Let denote the amount of time (in seconds) by which the racer that started in the insider position is ahead when 100t percent of the race has been completed, and suppose that  , can be effectively modeled as a Brownian Motion process with variance parameter .

, can be effectively modeled as a Brownian Motion process with variance parameter .

6. First Passage Time

Let  denote the first time that standard Brownian motion hits level a (starting at X(0) = 0), assuming a >0, then we have

denote the first time that standard Brownian motion hits level a (starting at X(0) = 0), assuming a >0, then we have

: you know that at some time before t, the process hits a. From that point forward, you are just as likely to be above a as below a.

: you know that at some time before t, the process hits a. From that point forward, you are just as likely to be above a as below a.  : cannot be above a, because the first passage time to a is after t.

: cannot be above a, because the first passage time to a is after t.

Thus,

,

.

Change variables:  , we have

, we have  .

.

By symmetry, we get  .

.

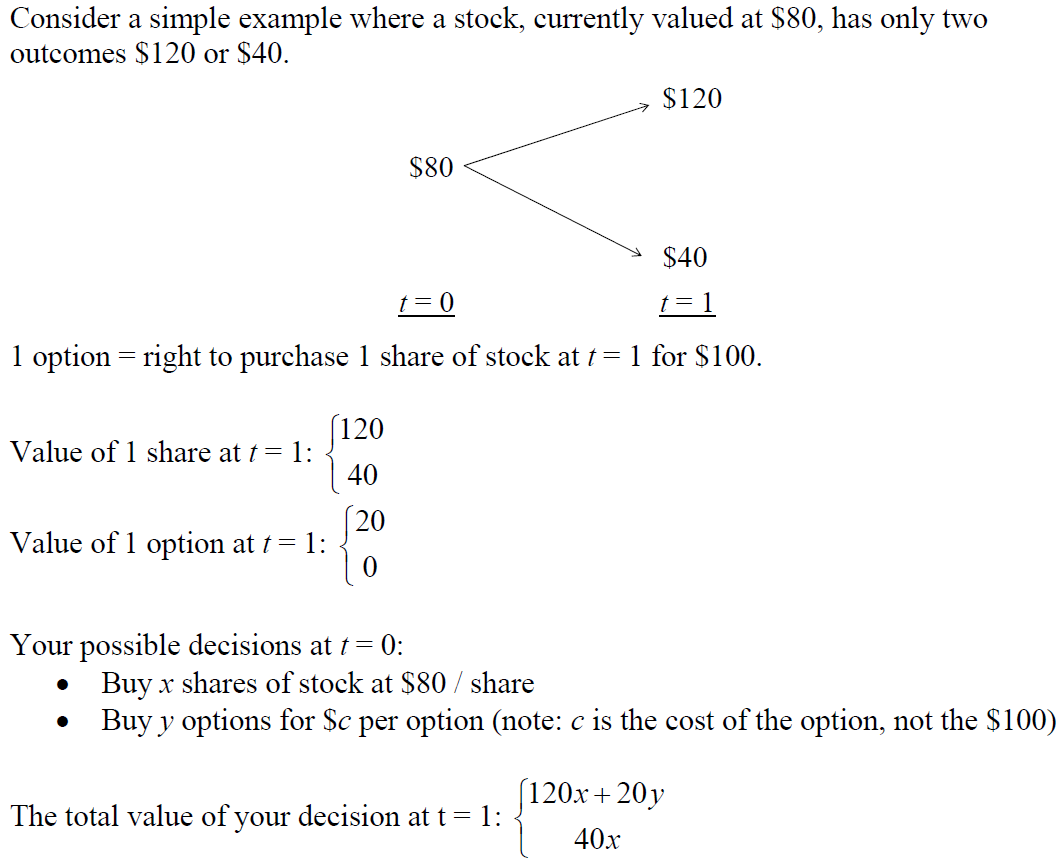

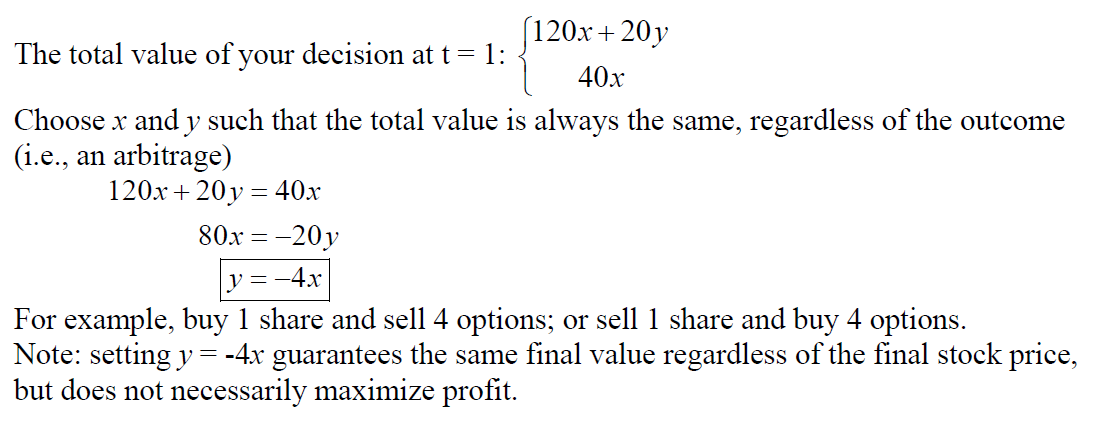

on m possible outcomes:

on m possible outcomes:  .

. to be the outcome of wagers i if outcome j occurs.

to be the outcome of wagers i if outcome j occurs. , then

, then  is earned if outcome j occurs.

is earned if outcome j occurs. such that

such that  ,

,

such that

such that

. Then

. Then  is geometric Brownian motion.

is geometric Brownian motion. be the price of a stock at time

be the price of a stock at time  (where n is distance); Let

(where n is distance); Let  be the fractional increase/decrease in the price of the stock from time n-1 to time n.

be the fractional increase/decrease in the price of the stock from time n-1 to time n. are i.i.d. Then

are i.i.d. Then

looks like a random walk.

looks like a random walk.![E[Y(t) | Y(s) = y_s] = y_s E[e^{{X(t) - X(s)}}]](http://mytechroad.com/wp-content/ql-cache/quicklatex.com-6123dcd406e7c3169967714c004b40f9_l3.png "Rendered by QuickLaTeX.com")

![E[Y(t) | Y(s) = y_s] = E[e^{X(t)} | X(s) = ln y_s]](http://mytechroad.com/wp-content/ql-cache/quicklatex.com-701e5d1e797fb903bd2750dec8a1eed7_l3.png "Rendered by QuickLaTeX.com")

![E[e^{X(t) - X(s) + X(s)} | X(s) = ln y_s]](http://mytechroad.com/wp-content/ql-cache/quicklatex.com-cbaa4bc6913e4710b685d37a0c9ed632_l3.png "Rendered by QuickLaTeX.com")

![y_s E[e^{X(t) - X(s)}]](http://mytechroad.com/wp-content/ql-cache/quicklatex.com-8719921d7edc09270eaaf88041d3ce07_l3.png "Rendered by QuickLaTeX.com")

, then

, then  is lognormal with mean

is lognormal with mean ![E[e^W] = e^{mu + sigma^2/2}](http://mytechroad.com/wp-content/ql-cache/quicklatex.com-8f034b090dfb3a6326d07789f19c1cc4_l3.png "Rendered by QuickLaTeX.com")

![N[mu(t-s), sigma^2(t-s)]](http://mytechroad.com/wp-content/ql-cache/quicklatex.com-fe97cb2671709fb45d594be3e856395c_l3.png "Rendered by QuickLaTeX.com") , since

, since  , then

, then ![E[Y(t)|Y(0) = y_0 ] = y_0 e^{sigma^2 t/2}](http://mytechroad.com/wp-content/ql-cache/quicklatex.com-9a556a5f4b14c08ba70ffb8439f32f49_l3.png "Rendered by QuickLaTeX.com") . Thus

. Thus ![E[Y(t)]](http://mytechroad.com/wp-content/ql-cache/quicklatex.com-81766f2a95bfc8f5b83bea45159b759f_l3.png "Rendered by QuickLaTeX.com") is increasing even though the jump process with

is increasing even though the jump process with  , where

, where  where

where

assuming the intervals of

assuming the intervals of ![[t_1,t_2]](http://mytechroad.com/wp-content/ql-cache/quicklatex.com-2b75109efb608046e3568b2e8579ce71_l3.png "Rendered by QuickLaTeX.com") and

and ![[t_3,t_4]](http://mytechroad.com/wp-content/ql-cache/quicklatex.com-e40d919d6ced58cec8bed1c6436689fa_l3.png "Rendered by QuickLaTeX.com") are disjoint.

are disjoint. .

.

, then

, then ![V[Y(t)] = 1](http://mytechroad.com/wp-content/ql-cache/quicklatex.com-b46d4b1bc9a9c3b2fa598be1e1736931_l3.png "Rendered by QuickLaTeX.com") .

.