1. Introduction

Definition: the simultaneous buying and selling of securities, currency, or commodities in different markets or in derivative forms in order to take advantage of differing prices for the same asset.

2. Option Pricing

Question:

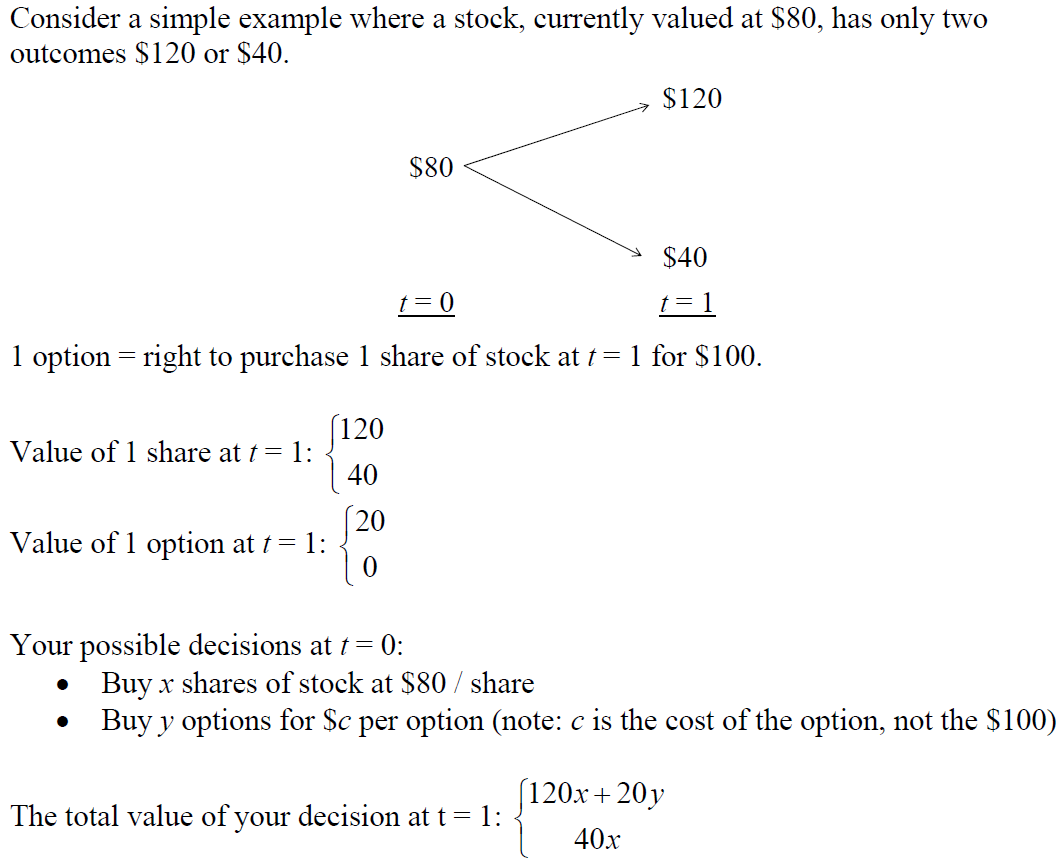

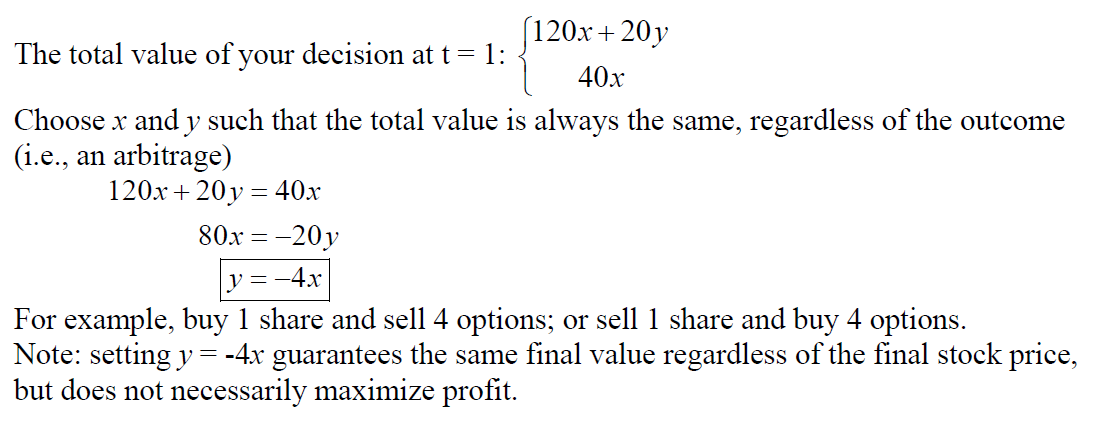

How to choose x and y:

How to maximize profit:

Key Assumption: There is no limit to buying or selling of options. In practice,

you may only be able to buy, but no sell, for example.

3. Aibitrage Theorem

Definition:

Consider n possible wagers  on m possible outcomes:

on m possible outcomes:  .

.

Let  to be the outcome of wagers i if outcome j occurs.

to be the outcome of wagers i if outcome j occurs.

If  is bet on wager

is bet on wager  , then

, then  is earned if outcome j occurs.

is earned if outcome j occurs.

Arbitrage Theorem:

such that

such that  ,

,

such that

such that

Intuitively,

- First theorem: there is a probability vector such that the expected outcome of every bet is 0, or

- There existing a betting scheme that leads to a sure win.

## TODO: explain more about these two theorem