Excess Distribution of Renewal Process

– Course notes of Stochastic Process, 2014 Fall

1. Definition

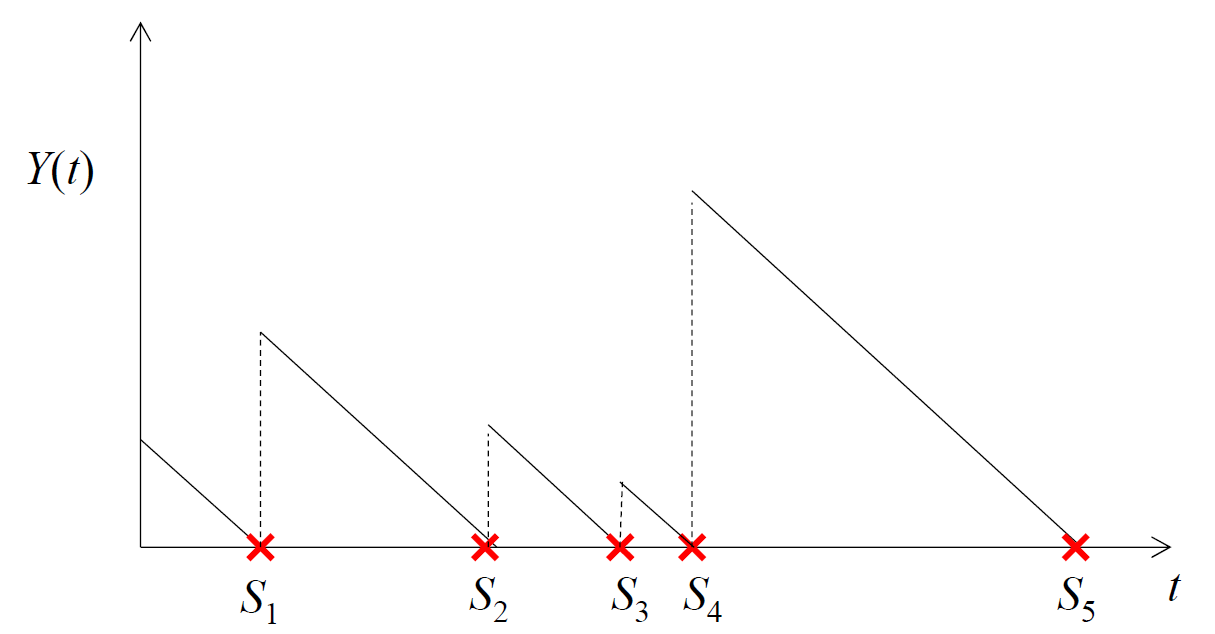

Excess of renewal process is defined as  (time until next event)

(time until next event)

(time until next event)

In the example of average time waiting bus, we drived

![lim_{t to infty} frac{int^T_0 Y(u)du}{T} = frac{E[X_n]}{2} + frac{car[X_n]}{2E[X_n]}](http://mytechroad.com/wp-content/ql-cache/quicklatex.com-750059cd2171990272f7cc9875c65d06_l3.png "Rendered by QuickLaTeX.com")

Now we are going to derive  for a random

for a random  .

.

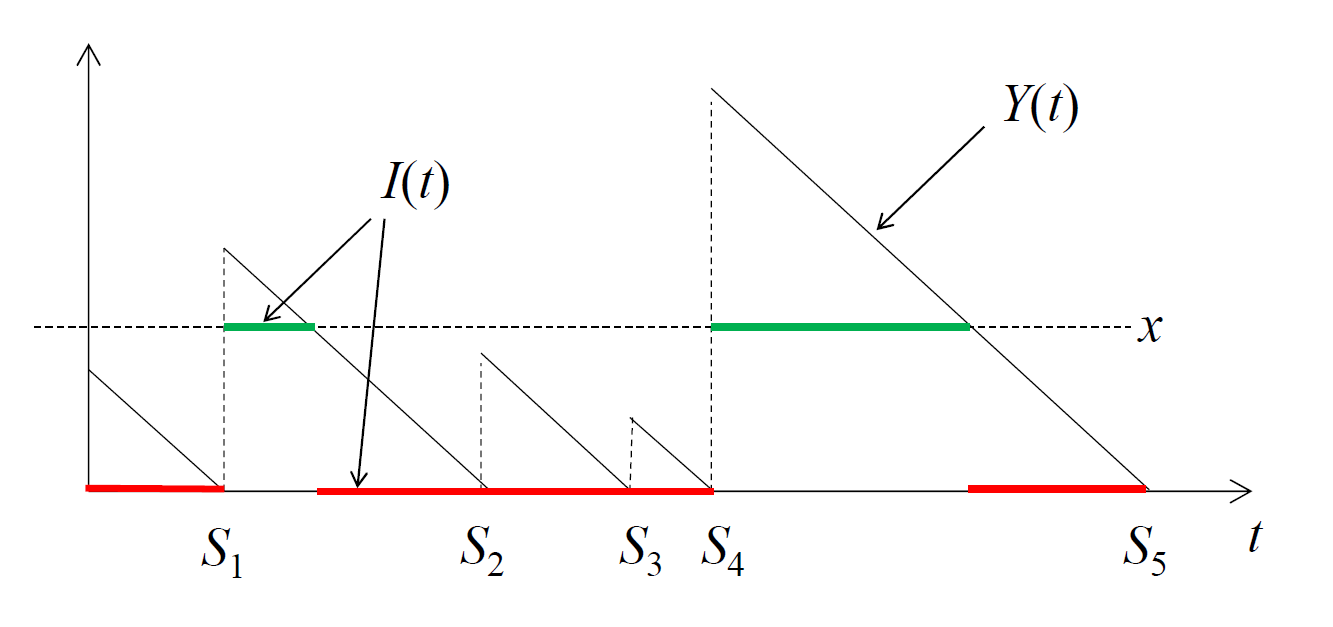

Interpretation: You show up “at random”. What is the probability that you wait more than x for the next event?

2. Derivation of

As we want to determine the fraction of time that  .

.

. Let  if , and let

if , and let  otherwise.

otherwise.

if , and let otherwise.

Interpretation: Fraction of time that = Fraction of “on” time for

= Fraction of “on” time for Let  be “on” time during cycle

be “on” time during cycle  , then

, then

be “on” time during cycle , then  if

if

otherwise

otherwise

Note: the ON time and OFF time for each cycle are dependent. A longer ON time implies a shorter OFF time.

Then we have

![E[Z_j] = E[max(X_j -x, 0)] = int^{infty}_0 Pr(max(X_j- x, 0) > u) du](http://mytechroad.com/wp-content/ql-cache/quicklatex.com-0d19b8e007f6d8406f88bba2bdc275d5_l3.png "Rendered by QuickLaTeX.com")

=

=

=

Since is an alternating renewal process, fraction of “on” time is

is an alternating renewal process, fraction of “on” time is![frac{E[Z_j]}{E[X_j]} = frac{1}{E[X_j]} int^{infty}_x F^c(u) dy](http://mytechroad.com/wp-content/ql-cache/quicklatex.com-327a52174f5e31964a02c2cd7cf2b0b3_l3.png "Rendered by QuickLaTeX.com")

This is sometimes called equilibrium distribution,

3. Example of different distribution of

Example:  ~ exp

~ exp

~ exp

=

As expected (by memoryless property), excess distribution is an exponential distribution.

Example: Pareto Distribution

is also called the tail distribution

is also called the tail distributionSome properties: ![E[X_j ] = frac{1}{alpha}](http://mytechroad.com/wp-content/ql-cache/quicklatex.com-227d4cb85491bbc153e8a45a7d34074a_l3.png "Rendered by QuickLaTeX.com") (mean only exist if

(mean only exist if

(mean only exist if ![Pr(Y(t) > x) = frac{1}{E[X_j]} int^{infty}_x F^c(u) du = (1+x)^{-(alpha-1)}](http://mytechroad.com/wp-content/ql-cache/quicklatex.com-a8f46c083d2b1d1494dd6f06a9a7f5a3_l3.png "Rendered by QuickLaTeX.com")

Example: Deterministic

– Assume  if

if  , otherwise

, otherwise  .

.

if , otherwise .![Pr(Y(t) geq x) = frac{1}{E[X_j]} int^{infty}_x F^c(mu) dmu](http://mytechroad.com/wp-content/ql-cache/quicklatex.com-177cc236dd82b51cfe78fb2c11aa1701_l3.png "Rendered by QuickLaTeX.com")

=

=

This is the CCDF of a uniform distribution on ![[0,D]](http://mytechroad.com/wp-content/ql-cache/quicklatex.com-d4e9347560fc995f60d5b13526ac2e73_l3.png "Rendered by QuickLaTeX.com") .

.

.Note: the above assume that  , If

, If  , then the result is 0.

, then the result is 0.

, If , then the result is 0. ON time of cycle j

ON time of cycle j OFF time of cycle j

OFF time of cycle j

must satisfy the following property in order for

must satisfy the following property in order for  must be i.i.d; in particular,

must be i.i.d; in particular,  for

for  . That is

. That is .

.![frac{mbox{average up time in a cycle}}{mbox{average time of one cycle}} = frac{E[Z_j]}{E[Z_j] + E[Y_j]}](http://mytechroad.com/wp-content/ql-cache/quicklatex.com-91c0a0a4e02573898c5cda2130078edf_l3.png "Rendered by QuickLaTeX.com")

.

.  of cars are speeding (>10 mph over the pretend speed limit). Assume time to issue a ticket~UNIF[10,14] minutes(one officer)

of cars are speeding (>10 mph over the pretend speed limit). Assume time to issue a ticket~UNIF[10,14] minutes(one officer) per min.

per min.![frac{E[Z_j]}{E[Z_j] + E[Y_j]} = frac{12}{12+5/2} = frac{12}{14.5}](http://mytechroad.com/wp-content/ql-cache/quicklatex.com-d61b2b73aff0c70206695975f48481f8_l3.png "Rendered by QuickLaTeX.com")

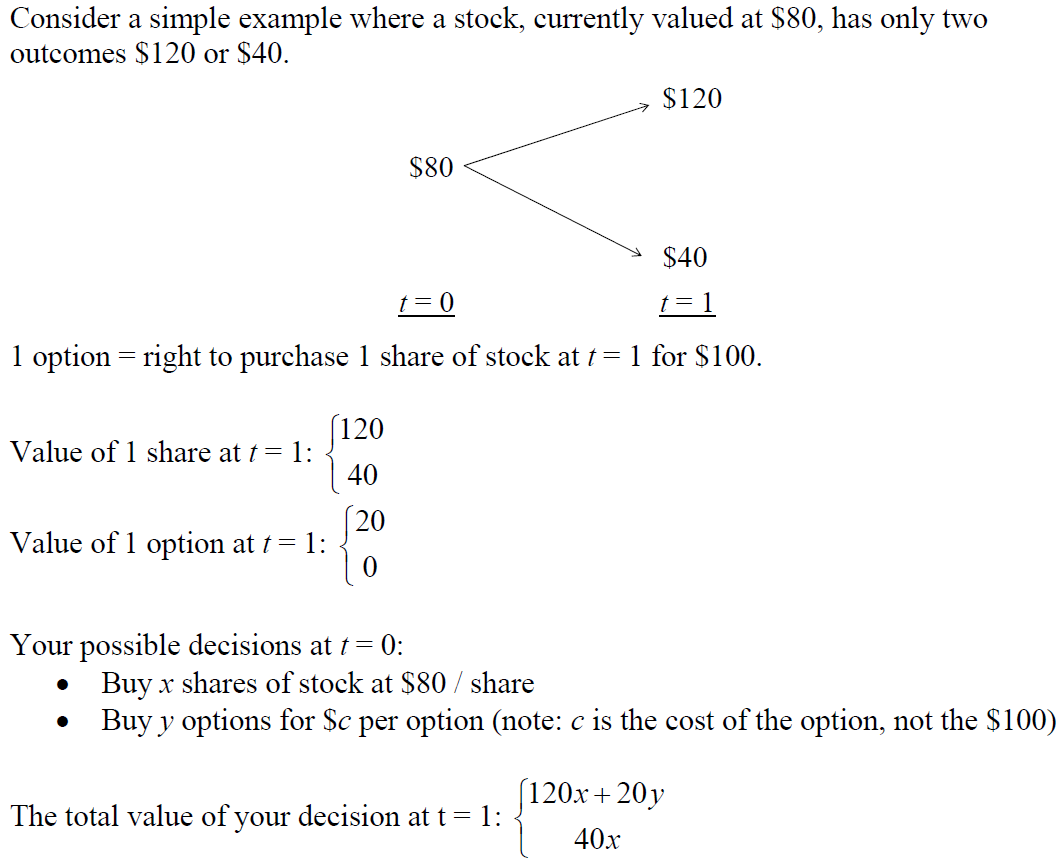

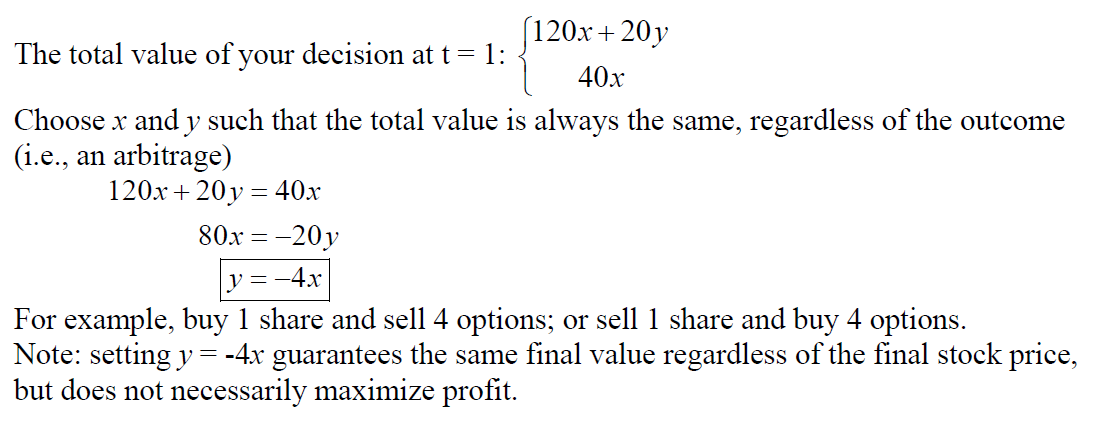

be the price of a stock at time s, considered on a time horizon

be the price of a stock at time s, considered on a time horizon ![s in [0,t]](http://mytechroad.com/wp-content/ql-cache/quicklatex.com-a762adbae0fb6065ce545731c1dcb638_l3.png "Rendered by QuickLaTeX.com") . The following actions are available:

. The following actions are available: , you can buy or sell shares of stock for

, you can buy or sell shares of stock for

, there are N options available. The cost of option

, there are N options available. The cost of option  is

is  per option which allows you to purchase

per option which allows you to purchase  share at time

share at time  for price

for price  .

. , where

, where  .

.

![E[e^{-alpha t} X(t) | X(s)] = e^{-alpha t} X(s) e { mu/(t-s) + frac{sigma^2(t-s)}{2}}](http://mytechroad.com/wp-content/ql-cache/quicklatex.com-12ddc47252af565aed0785998a1baf5e_l3.png "Rendered by QuickLaTeX.com")

such that

such that

![E[e^{-alpha t} X(t) | X(s)] = e^{-alpha t} X(s) e^{-alpha(t-s)} = e^{-alpha s} X(s)](http://mytechroad.com/wp-content/ql-cache/quicklatex.com-5f9bdae01a64793ac51fed04f2eed82f_l3.png "Rendered by QuickLaTeX.com") .

.![- c + E[max (e^{alpha t} X(t)- k), 0]](http://mytechroad.com/wp-content/ql-cache/quicklatex.com-a9cb06d5f71316f190c3485fd436505c_l3.png "Rendered by QuickLaTeX.com")

![-c + E[e^{-alpha t} (X(t) - k)^+]](http://mytechroad.com/wp-content/ql-cache/quicklatex.com-0e6064bae2e4f52212c1a87c8be915e9_l3.png "Rendered by QuickLaTeX.com")

![ce^{alpha t} = E[ (X(t) - k)^+] = E[(x_0 e^{Y(t)} - k)^+]](http://mytechroad.com/wp-content/ql-cache/quicklatex.com-fc5742e0bd281ec47bddd20ecce7594a_l3.png "Rendered by QuickLaTeX.com")

has value 0 when

has value 0 when  , i.e., when

, i.e., when

, i.e.,

, i.e.,

, cost of option is

, cost of option is

, cost of option is

, cost of option is

increase, c increase (assuming

increase, c increase (assuming  )

) , c decreases

, c decreases

on m possible outcomes:

on m possible outcomes:  .

. to be the outcome of wagers i if outcome j occurs.

to be the outcome of wagers i if outcome j occurs. is bet on wager

is bet on wager  is earned if outcome j occurs.

is earned if outcome j occurs. such that

such that  ,

,

such that

such that

and variance parameter

and variance parameter  . Let

. Let  . Then

. Then  is geometric Brownian motion.

is geometric Brownian motion. be the price of a stock at time

be the price of a stock at time  (where n is distance); Let

(where n is distance); Let  be the fractional increase/decrease in the price of the stock from time n-1 to time n.

be the fractional increase/decrease in the price of the stock from time n-1 to time n. are i.i.d. Then

are i.i.d. Then

looks like a random walk.

looks like a random walk.![E[Y(t) | Y(s) = y_s] = y_s E[e^{{X(t) - X(s)}}]](http://mytechroad.com/wp-content/ql-cache/quicklatex.com-6123dcd406e7c3169967714c004b40f9_l3.png "Rendered by QuickLaTeX.com")

![E[Y(t) | Y(s) = y_s] = E[e^{X(t)} | X(s) = ln y_s]](http://mytechroad.com/wp-content/ql-cache/quicklatex.com-701e5d1e797fb903bd2750dec8a1eed7_l3.png "Rendered by QuickLaTeX.com")

![E[e^{X(t) - X(s) + X(s)} | X(s) = ln y_s]](http://mytechroad.com/wp-content/ql-cache/quicklatex.com-cbaa4bc6913e4710b685d37a0c9ed632_l3.png "Rendered by QuickLaTeX.com")

![y_s E[e^{X(t) - X(s)}]](http://mytechroad.com/wp-content/ql-cache/quicklatex.com-8719921d7edc09270eaaf88041d3ce07_l3.png "Rendered by QuickLaTeX.com")

, then

, then  is lognormal with mean

is lognormal with mean ![E[e^W] = e^{mu + sigma^2/2}](http://mytechroad.com/wp-content/ql-cache/quicklatex.com-8f034b090dfb3a6326d07789f19c1cc4_l3.png "Rendered by QuickLaTeX.com")

![N[mu(t-s), sigma^2(t-s)]](http://mytechroad.com/wp-content/ql-cache/quicklatex.com-fe97cb2671709fb45d594be3e856395c_l3.png "Rendered by QuickLaTeX.com") , since

, since  , then

, then ![E[Y(t)|Y(0) = y_0 ] = y_0 e^{sigma^2 t/2}](http://mytechroad.com/wp-content/ql-cache/quicklatex.com-9a556a5f4b14c08ba70ffb8439f32f49_l3.png "Rendered by QuickLaTeX.com") . Thus

. Thus ![E[Y(t)]](http://mytechroad.com/wp-content/ql-cache/quicklatex.com-81766f2a95bfc8f5b83bea45159b759f_l3.png "Rendered by QuickLaTeX.com") is increasing even though the jump process with

is increasing even though the jump process with  , where

, where  is standard Brownian Motion.

is standard Brownian Motion. where

where

.

. with probability

with probability  and

and ![E[X_i] = 0](http://mytechroad.com/wp-content/ql-cache/quicklatex.com-f8aaebca6a792a3c1f96703c49cc3f67_l3.png "Rendered by QuickLaTeX.com") and

and ![Var[X_i] = E[X^2_i] - E[X_i]^2 = 1](http://mytechroad.com/wp-content/ql-cache/quicklatex.com-1b4a23e17c1ffe9311f56a51f18e7bb9_l3.png "Rendered by QuickLaTeX.com") .

.

denote the state of Markov Chain after n jumps, then

denote the state of Markov Chain after n jumps, then

![E[X(t)] = 0](http://mytechroad.com/wp-content/ql-cache/quicklatex.com-5521d8e7a8c3e27e09dae171218efa5f_l3.png "Rendered by QuickLaTeX.com") and

and ![Var[X(t)] = (Delta x)^2 cdot frac{t}{Delta t}](http://mytechroad.com/wp-content/ql-cache/quicklatex.com-0f44ab27f24a965379568a8548d9ea92_l3.png "Rendered by QuickLaTeX.com") .

. , then

, then![V[X(t)] = (Delta x)^2 cdot frac{t}{Delta} to sigma^2 t](http://mytechroad.com/wp-content/ql-cache/quicklatex.com-fb1f4cf9dd65e73704e883268ac9c80c_l3.png "Rendered by QuickLaTeX.com") .

.

is independent of

is independent of  assuming the intervals of

assuming the intervals of ![[t_1,t_2]](http://mytechroad.com/wp-content/ql-cache/quicklatex.com-2b75109efb608046e3568b2e8579ce71_l3.png "Rendered by QuickLaTeX.com") and

and ![[t_3,t_4]](http://mytechroad.com/wp-content/ql-cache/quicklatex.com-e40d919d6ced58cec8bed1c6436689fa_l3.png "Rendered by QuickLaTeX.com") are disjoint.

are disjoint. .

. .

.

, then

, then ![V[Y(t)] = 1](http://mytechroad.com/wp-content/ql-cache/quicklatex.com-b46d4b1bc9a9c3b2fa598be1e1736931_l3.png "Rendered by QuickLaTeX.com") .

. , then

, then  .

.  has stationary and independent increments

has stationary and independent increments

and drift

and drift  . What is

. What is  Pr{X(30) >0 | X(10) = -3}

Pr{X(30) >0 | X(10) = -3} Pr{X(30) – X(20) >3 | X(10) =3 }

Pr{X(30) – X(20) >3 | X(10) =3 } Pr{X(20) – X(0) >3 }

Pr{X(20) – X(0) >3 } Pr{X(20)>3 }

Pr{X(20)>3 } Pr{N(2,80) > 3} = Pr{X(0,1) > frac{3-2}{sqrt{80}}

Pr{N(2,80) > 3} = Pr{X(0,1) > frac{3-2}{sqrt{80}} 1-Phi(frac{1}{4sqrt{5}})

1-Phi(frac{1}{4sqrt{5}}) X(s) = x | X(t) = B

X(s) = x | X(t) = B frac{s}{t} cdot B

frac{s}{t} cdot B frac{s}{t} cdot (t-s)

frac{s}{t} cdot (t-s) s = t/2

s = t/2 X(t)

X(t) N(0, sigma^2 t)

N(0, sigma^2 t) 10 after 6 hours, what is the probability that the stack was above its starting value after 3 hours?

10 after 6 hours, what is the probability that the stack was above its starting value after 3 hours?

~

~  =

=  .

.

, can be effectively modeled as a Brownian Motion process with variance parameter

, can be effectively modeled as a Brownian Motion process with variance parameter

denote the first time that standard Brownian motion hits level a (starting at X(0) = 0), assuming a >0, then we have

denote the first time that standard Brownian motion hits level a (starting at X(0) = 0), assuming a >0, then we have

: you know that at some time before t, the process hits a. From that point forward, you are just as likely to be above a as below a.

: you know that at some time before t, the process hits a. From that point forward, you are just as likely to be above a as below a.  :

:  ,

,  .

. , we have

, we have  .

. .

.